TSMC’s Heroic Assumption – Low Utilization Rates, Fab Cancellation, 3nm Volumes, Automotive Weakness, AI Advanced Packaging Demands, 2024 Capex Weakness

Can these heroic assumptions be supported? Tremendous risk.

TSMC reported their Q1 earnings, and as the heart of the semiconductor industry, following them closely means you are reading the pulse. While many other companies can help give signs and indications, no one else is quite in the center of it all, like TSMC.

Today, we unpack TSMC’s action-packed quarterly earnings and update our readers on everything that is happening here. This includes talking about datacenter, mobile, and automotive semiconductor markets. There are now signs of weakness in automotive, which was the last holdout of strength in the market. On the optimistic side, TSMC talked about receiving a huge order 2 days ago for an AI chip.

TSMC also talked about a fab cancellation and how an expansion is now no longer financially feasible. We will be sharing some of our data about TSMC’s utilization rates and how TSMC’s pricing is coming down. We dive deep into TSMC’s 3nm and 5nm ramps as there are some quite heroic assumptions that TSMC is making regarding those in the back half of the year.

Revenue Walk

The headline number for the quarter was that revenue was down to $16.72 billon for Q1 2023, down 4.8% year on year. Furthermore, TSMC’s Q2 guidance implies the picture gets much worse and falls to $15.6 billion at the midpoint, a 14.6% decrease year on year. With that said, TSMC shared their full year guidance, which allows us to back into the following estimates. We will share more on this later with regard to 5nm and 3nm ramps.

High-performance computing continues to grow as a percentage of revenue from 42% to 44% of the company’s revenue. While the datacenter is strong, especially with AMD Genoa, Nvidia H100, and Amazon Graviton 3 ramps as standouts, it should be noted even low-power laptop chips such as Apple’s M1 are included in the high-performance computing segment.

Despite growing as a percentage of revenue, in absolute dollar terms, the segment shrank by $1 billion, 27% quarter on quarter. The smartphone picture looked the worst, with sales declining $1.8 billion for the quarter and also declining for the year. IoT continued to be strong with year-on-year growth despite quarterly weakness.

Automotive was the standout. It grew ~50% year on year! This sounds great for most automotive suppliers, such as NXP, Onsemi, Infineon, and ST Micro, but it wasn’t all pretty.

While automotive demand is holding steady for TSMC and it is showing signs of softening into second half of 2023.

C.C Wei, TSMC CEO

This confirms the view we shared with clients 2 months ago on flipping underweight $ON.

Utilization Rates Plummet

Utilization rates are one of the most important numbers in the semiconductor business. Given the business is so capital intensive, time spent idle is time spent lighting money on fire. TSMC had a big revenue and gross margin hit primarily due to its low utilization rates this quarter. TSMC has enjoyed 100% utilization rates since the Covid boom started. Now the picture isn’t so pretty.

Q4 2022 showed the first signs of weakening and shipment cuts, but they are in full swing now. TSMC’s N7 (7nm) class node is the worst affected as far as utilization rates go. Last quarter we pointed out they were running at ~83% utilization rates.

Now, SemiAnalysis data indicates that the 7nm utilization rates were below 70% in Q1! Furthermore, Q2 gets even worse, with 7nm utilization rates falling to below 60%! This is primarily due to weakness in both smartphones and PCs, but there is a broader weakness in most segments.

7nm was not the only node that was affected. N16 also fell below 90% utilization in Q1 and looks to be at ~75% utilization in Q2. Even N5 is affected, with utilization rates around 88%. Despite TSMC N5 being the best process technology node, far ahead of Samsung and Intel even 3 years after its initial shipments, it is not invulnerable to the semiconductor business’s cyclicality. TSMC’s older nodes remained strong, although there were some signs of weakening, and they begin to free up capacity in Q2.

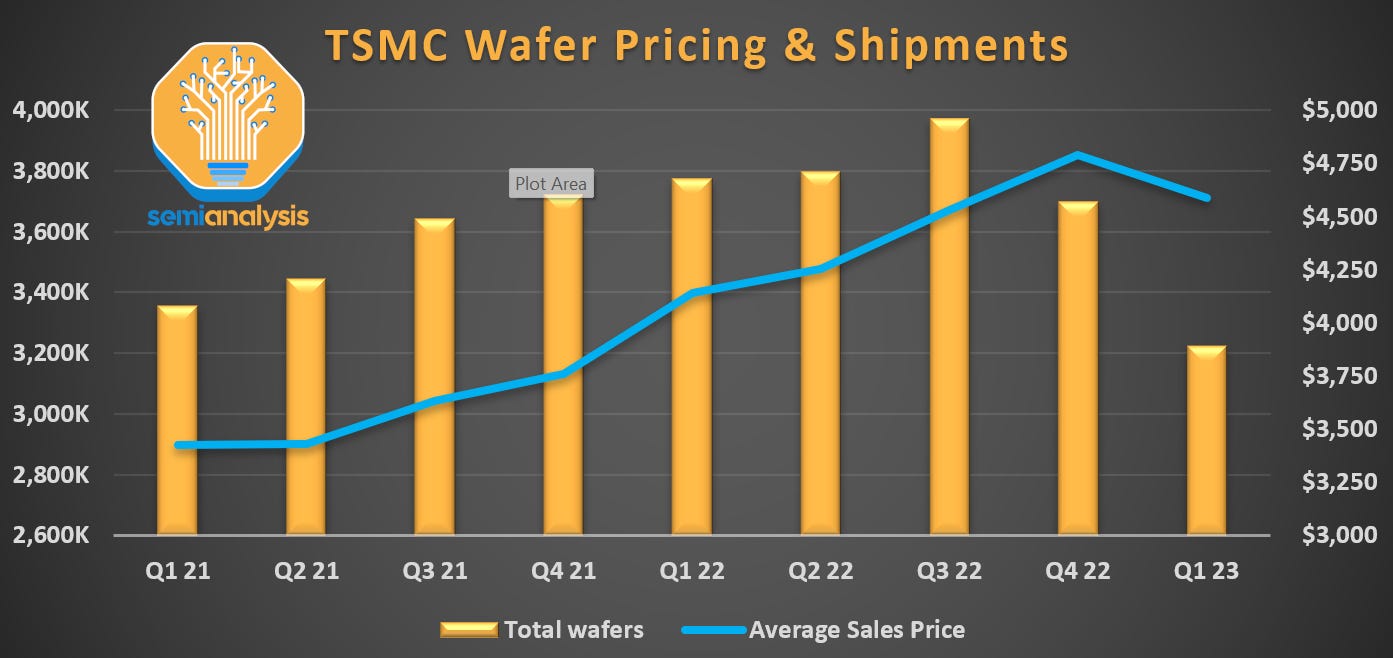

TSMC Pricing Declines

TSMC’s pricing has declined for the first time in many years. Even though wafer shipments fell from nearly 4 million wafers a quarter to 3.7 million in Q4 2022, pricing continues to increase. In Q1 2023, shipments continued to tank to 3.2 million.

This pricing decrease is mostly a result of poor utilization of TSMC’s N7 process node family. TSMC is not reducing pricing to customers in 2023. We have multiple major fabless firms who confirm this for both trailing edge and 5nm class nodes.

3nm & 2nm Update

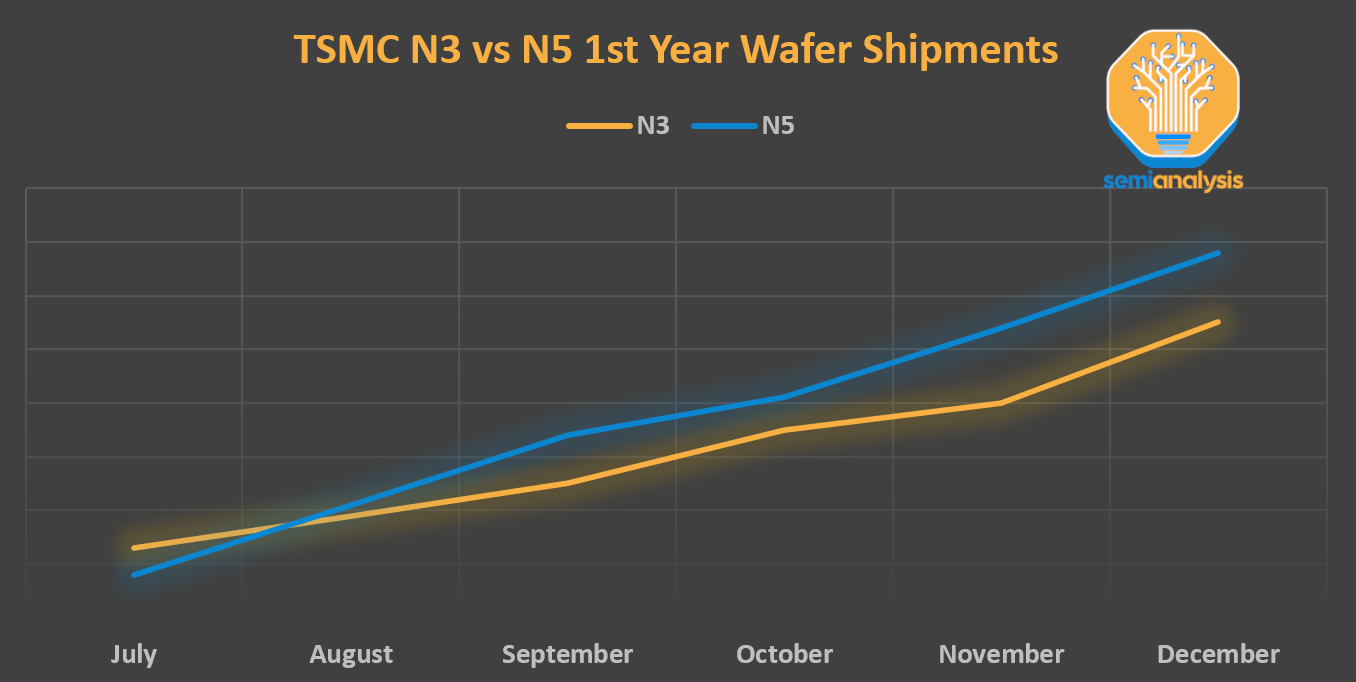

TSMC reiterated their statements given in previous quarters surrounding their future nodes, N3 and N2. N3 demand exceeds supply and will make up mid-single digits of full-year 2023 revenue, with a sizeable contribution from Q3. As with new node introductions, N3 will dilute gross margins in the initial phase of the volume ramp.

This is exacerbated by N3’s slower ramp and smaller wafer volumes compared to N5 in their respective first year of shipments. Apple’s recent change of including the latest chip only on the Pro models and the much higher ASP per N3 wafer vs N5 indicates that the wafers per month (WPM) ramp on N3 will trail N5 by some margin.

Following on, the relaxed N3E variant is set to commence volume production in the 2nd half of 2023. This is the main 3nm variant being adopted by most customers. TSMC is seeing strong engagement on 3nm, with more than double the chip design tape-outs vs 5nm in the first 2 years of introduction.

A big contributor to this is the tightening gap between smartphone and HPC product ramps. Historically, smartphones were the first to ramp new nodes, as small die sizes of phone chips helped with yields. Now, with the advent of chiplets and the insatiable demand for power efficiency in the datacenter, many HPC customers are clamoring to get their products on 3nm as soon as possible.

N2, their 1st attempt at nanosheets, is still expected to enter volume production in 2025, with a much higher revenue contribution from 2026. N2 will deliver a full node worth of performance and power benefit over N3. While not commenting on competitors, TSMC expects its N3 node to be the most advanced in the industry, and they are fully confident that N2 will continue to extend its technology leadership in the future.

Our 2-nanometer technology will be the most advanced semiconductor technology in the industry, in both density and energy efficiency when it is introduced and will further extend our technology leadership well into the future.

C.C Wei, TSMC CEO

Let’s see if Intel’s 18A has anything to say about this. Volumes TSMC will retain leadership but the technology crown maybe not. We wrote extensively about a portion of the 18A process here.

28nm Cancellation

TSMC is wary of oversupply in lagging edge nodes and are thus focusing on expanding capacity for specialty technologies like RF and imaging. Their Kaohsiung fab was supposed to be expanded with more 28nm capacity, but that is no longer financially feasible. The focus for expansion has now shifted to the leading edge.

So we built one in Japan, we're also expanding our 28nm capacity in Nanjing, that's the 2nd one, and then we're considering Europe, that might be the 3rd one for automotive application. Put all three together, we don't think today that Kaohsiung, if we build 28nm, probably, it won't be financially feasible. So we adjusted to become a more advanced node, which we are still in shortage.

C.C Wei, TSMC CEO

Overseas Fabs

TSMC gave a progress update on their overseas fab buildouts, now led by the Overseas Operations Office (OOO), whose task is to ensure each fab’s culture remains coherent across countries and to provide support to ensure fab performance matches those in Taiwan.

The US fab in Arizona faced some permit issues but is still expected to produce chips on the N4 process from late 2024. While costs are definitely higher than in Taiwan, TSMC believes the geographic location provides value to customers and will be selling on this value. This means customers are willing to pay more per wafer if it comes from the US fab. Hence, margins are expected to be in line with the company average.

TSMC’s specialty 28nm fab in Japan is also expected to commence volume production by late 2024. They are also expanding their 28nm fab in Nanjing, China to support their customers there. Finally, TSMC is assessing the feasibility of a 28nm fab in Europe for automotive customers, pending on customer feedback and government support. TSMC also pointed out that they have hired more than 900 US staff for their Arizona fab, and more than 370 in Japan, but that pales in comparison to the 6000+ hirings in 2023 alone in Taiwan.

Capex Trail Off

One of the most important numbers is that TSMC said their capital spending in 2023. They reiterated their prior shared figure of $32B to $36B, down from $36.4B in 2022. This is especially interesting because of prior reports from Taiwan media that Capex was being cut and pushed out by as much as 40%! The same outlet also said N5 utilization was back to full in Q2, which is clearly not true either. Yet another reminder that this outlet is nothing more than a tabloid.

TSMC reiterating Capex makes complete sense, given the spending profile of their Capex. They spent $9.95 billion in the first quarter, nearly 30% of the year’s budget. We believe that Q2 will be large as well, around $9B, although not quite $10 billion like in Q1. This would mean TSMC’s Capex run rate in the first half is ~$38 billion.

Of course, TSMC is not spending much in 2024. Furthermore, TSMC is not ordering heavily for 2024 either. They have been cautiously optimistic in that regard. Look no further than ASML, the lithography champion, and 2nd largest tool manufacturer after Applied Materials.

ASML only had €3.75B of new orders in Q1 (O/w EUV €1.6B) despite revenue €6.75B. This tremendous weakness in orders is not going to affect 2023, but rather 2024. ASML and SemiCap, in general, will enjoy a very strong 2023 thanks to large orders placed last year, plus China rushing to ship huge amounts of tools in. For example, China is purchasing 45% of the DUV tools ASML makes before any further bans come in. SMIC is rushing to expand their 7nm process technology rapidly with these tools.

With that tangent put aside, indications of weak orders fuel our view that TSMC’s Capex will fall off. TSMC’s H2 Capex run rate is closer to $30 billion. This has very negative implications for firms like ASML, Applied Materials, Lam Research, Screen, ASMI, KLA, Onto, and Nova Measurements. Despite current strength and hopes of continued growth through the year, there is a wake-up call coming later this year and early next year as Capex slows down.

All this capacity is being added to a shrinking market. If the semi-market doesn’t come roaring back, the capacity cycle will be very rough.

TSMC’s capital intensity, the amount spent on fabs vs revenue, is currently at ~46% in 2023. They commented on their long-term capital intensity coming in at mid-30% long-term. This would mean their Capex next year also lands in that ~$29B range, similar to their H2 2023 run rate for Capex. This could get ugly for SemiCap. They will all remain FCF positive, unlike memory players are currently, but the hope of memory rebound pushing SemiCap to new highs needs to be counterweighed with a leading edge slump and further China bans.

Advanced Packaging

TSMC guided for Advanced Packaging revenue to decline due to customer demand, from 7% of total revenue in 2022 to 6% to 7% for 2023. We stated this was happening last quarter. The reason is because fanouts for mobile are included in their advanced packaging bucket. Apple and especially MediaTek weakness here is the culprit.

That being said, the long-term growth rate is expected to be slightly higher than the corporate average. In terms of capacity expansion, the CEO had this to say:

Just recently in these 2 days I received a customer's phone call requesting a big increase on the backend capacity, especially in the CoWoS. We are still evaluating that.

C.C Wei, TSMC CEO

Nvidia is the largest customer of CoWoS for their A100 and H100 class datacenter AI GPUs. Google, through Broadcom, is the 2nd largest customer for TPUv4 and TPUv5. AMD also utilizes CoWoS in some capacity, but their volume in 2023 is relatively small. Lastly, Amazon’s Trainium through AlChip, as well as Microsoft’s new AI chips, also use CoWoS.

The demands of AI training on memory performance are pushing designs to use High Bandwidth Memory (HBM), which has to be connected using advanced packaging technologies such as CoWoS. Any one of these companies and, more likely all of them are increasing spending heavily and require more CoWoS capacity. To be clear, Amazon’s Tranium, despite big orders through Alchip, isn’t that great, and Microsoft’s 1st gen AI chip won’t be able to replace Nvidia either.

Heroic H2 Rebound?

TSMC’s full-year guidance means H2 is extremely strong. They are arguing that full-year revenue is down only low to mid-single digits; if we take a conservative estimate of down 3.9%, that lands full-year revenue at $72.92 billion. That doesn’t sound too crazy on a full-year basis. The problem is when you break out by quarter and node. Follow us into our dive into N5 and N3 ramp volumes.